[Contribution] Do optimists usually win?

One of the most over-used phrases of the past decade has been “buy-on-dips.” Many market analysts, including ourselves, have often reached for this phrase when considering the best course of action amid stock market volatility.

However, it raises a broader question of whether this optimism has been the right course of action. When faced with the choice of stocks or bonds, should investors have defaulted to buying equities on dips, or would they have been better served by seeking shelter in cash or high-quality bonds?

Do equity market optimists indeed make more money?

History shows that equity markets generally offer positive returns over the medium-to-longer term.

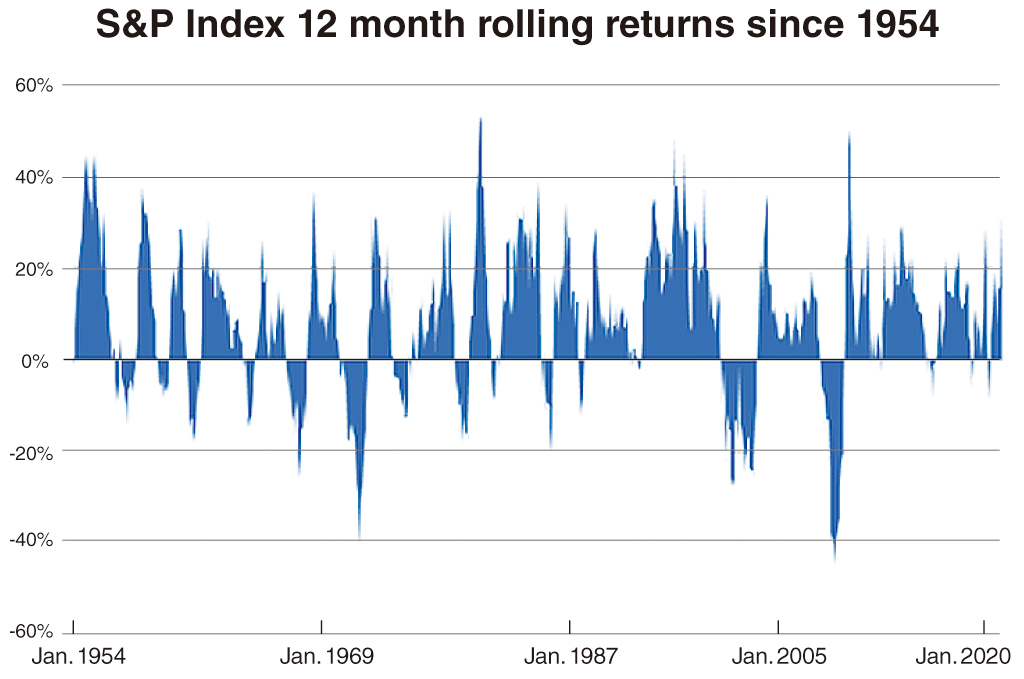

As the chart illustrates, over the past seven decades, 1-year returns on the S&P500 (chosen only for its long history) were positive a majority (about 74 percent) of the time. The period after the 2008-09 financial crisis paints an even more positive picture. Since 2009, 1-year returns were positive 84 percent of the time. These results don’t change significantly if one raises the bar to compare 1-year equity returns versus cash or investment grade bond returns.

We then asked ourselves how well a very simple buy-on-dips strategy performs. We imagined a first-time investor who is not confident of timing markets. The person decides to invest $100 in the S&P500 the first time the 12-month S&P500 return falls below that of cash (thus, just once during each continuous run of below-cash 12-month returns).

It turns out that, since 2010, the average 1-year return for such a strategy would have been 18 percent, handily beating the 12.3 percent average 12-month return on the S&P500.

If the same investor had been particularly unlucky and started this investing journey at the height of the internet bubble in 2000, only to be pummelled by two gut-wrenching recessionary sell-offs in 2000-2003 and 2008-2009, the average return of the allocations would have been lower at 8.8 percent. However, this still beats the 5.7 percent average 12-month return on the S&P500 over this period.

Needless to say, all of these were considerably higher than the average cash and investment grade bond returns.

Do we use ‘buy-on-dips’ as a rule then? Not quite a pessimist well-versed in renowned psychologist Daniel Kahneman’s “Thinking, Fast and Slow” would use the same data to remind us that, over the past seven decades, S&P500 12-month returns were negative 26 percent of the time.

Many of these periods were characterised by large drawdowns (more than 40 percent during the great financial crisis) or long-lasting equity bear markets (32 months of negative 1-year returns since November 2000).

It is not easy to stay the course with equities over such periods. Investors risk selling in error either because of behavioral reasons (panic) or technical reasons (how investments are structured). In such cases, while a dispassionate focus on returns alone may favor equities or other risky assets, a diversified allocation makes it easier to stay the course.

It is very natural that people are affected by behavioural biases when making decisions. In this case, negativity bias creeps in and we tend to pay much more attention to negativity, rather than positivity. It is, therefore, not surprising that we tend to pay a disproportionate amount of attention to prophets of doom.

The analysis of decades of market returns above suggests we should ignore the pessimists -– market drawdowns do occur, and many can challenge our staying power. However, investment allocations that realistically account for how much volatility each of us is able to handle before we risk making an investment error can help ensure we stay the course. This is where cash and bonds still play important roles as diversifiers and volatility mufflers.

History shows the “prepared” optimist is likely to indeed make more money than the pessimist.

By Manpreet Gill

Manpreet Gill is Head of FICC Strategy at Standard Chartered Wealth Management. Ed.

Words in this Article

volatility - n. the quality or state of being likely to change suddenly, especially by becoming worse

recessionary - adj. relating to a period, usually at least six months, of low economic activity, when investments lose value, businesses fail, and people lose their jobs

drawdown - n. a situation in which someone takes an amount of money that has been made available

allocation -n. the process of giving someone their part of a total amount of something to use in a particular way

disproportionate - adj. too large or too small in comparison to something else, or not deserving its importance or influence

Comprehension Quiz

What is the article mainly about?

Are you an optimistic person or a pessimistic person?

What can we know about 'buy-on-dips' rule?